High Cost Credit

Partner: Financial Regulatory body

Background

After the financial crash of 2008, high-cost, short-term credit (known as payday loans) became popular and loans were offered to consumers who had been denied more conventional forms of credit. However, these loans often left borrowers with unsustainable levels of debt, locked into multiple loans with spiralling charges and total repayments that far exceeded the original amount borrowed. For example, some loans were offered at interest rates that exceeded 5,000%.

Approach and Method

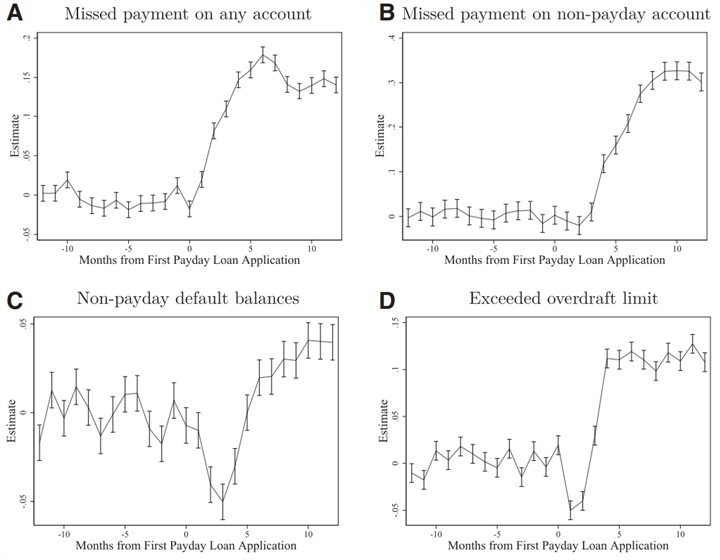

Drawing upon a unique database of over 15 million payday loan applications in the UK over a two-year period, the detail of the negative effects of payday loans on consumers was documented. Research showed (Gathergood, Guttman-Kenney & Hunt) that many of the consumers affected were among the most vulnerable individuals in society, as it was those who tended to use higher-cost credit products. The research directly helped shape the policy issued by the regulatory body, which took effect in January 2015.

Results

Acting to protect consumers who were applying for payday loans in the UK, the regulatory body introduced legislation to limit the prices that payday lenders could charge – in effect a price cap. This meant thousands of consumers saved more than £600 million in interest charges they would otherwise have had to pay. As a result of the policy, the default rate on loans also reduced and the Citizen’s Advice Services reported a 60% reduction in the number of individuals presenting with cases relating to payday loans.