Household and Estate Accounting

Domestic accounting was often done by the woman of the house. Notes about how much money was spent on household items could be written down in a variety of different ways, since the information was for private use and did not need to be read or necessarily understood by anybody else. Researchers therefore need to look carefully at household account books to decipher what was being recorded.

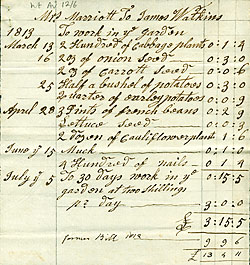

Account book, c.1804 (Wt C 6/6)

View larger version

Many archive collections contain examples of simple account books noting daily expenses and payments. The account book above was kept by Mrs Elizabeth Marriot, wife of Randolph Marriot. The Marriots took a lease on a house in Worcester in 1804, and also spent some time in Lyme Regis and Bath.

The page shown here lists household expenses in July 1804 including payments to the butcher and the grocer, and amounts spent on various food items including chickens, bacon, beans, candy, fish, fruit, lobster, tea, sugar etc. Such account books are idiosyncratic, and may not be complete or maintained for very long, but can give a very vivid idea of what a particular family was spending its money on during a particular period.

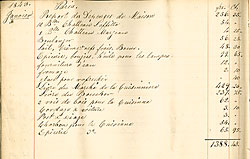

Account book of Lady William Bentinck's butler, 1843 (Pl F8/8/17)

View larger version

This is an example of a more formal account book drawn up by a household employee, Lady William Bentinck's butler Mr Oberst. It records domestic and other expenses at Lady William's house in Paris from January to May 1843. Its pages are divided into categories, 'Depenses de Maison' [domestic expenses] and 'Depenses Particullieres' [particular, or special expenses] for each month. An account of receipts is entered at the back of the volume. It is in French, and the amounts of money are francs and centimes. Domestic expenses included wine, food and spices; particular or special expenses included letters, medicine and charitable payments. The volume was checked and signed on 5 June 1843.

Not all accounts were kept in this linear way. The person in charge of the Mellish household at Blyth Hall, Nottinghamshire, chose to maintain a weekly overview of expenses. The household account book numbered Me H 1 is in the form of a grid. Different types of payment are categorised in rows, and the columns are made up of totals for each particular week. This logical and regular way of recording expenditure meant that comparisons could easily be made between particular weeks, or particular types of payment.

Estate accounts

Estate and manorial accounts were normally written in Latin until the late fifteenth or early sixteenth century. They also usually used Roman numerals instead of today's Arabic numerals. Mistakes were very common, since the figures could not be added up using modern arithmetic, and had to be done using an abacus before being transferred to the account.

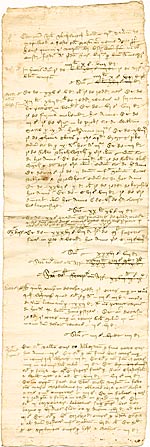

Compotus for the manor of Maplebeck, 1418-1419 (Ne M 144)

View larger version

Here is an example of the earliest surviving account in the Newcastle collection. It is a compotus (a manorial account) for the manor of Maplebeck in Nottinghamshire. It was drawn up by the bailiff, Robert Blithworth, and covers the period from the feast of St Martin 'in Yeme' [St Martin in Hyeme - 11 November] in the 6th year of the reign of King Henry V [1418], to the same feast in the following year [1419].

Compoti were usually written in a standard form. Like many others, this one begins with a list of arrears owing to the manor (abbreviated 'arr'), and rents paid to the manor (abbreviated as 'redd'), followed by lists of other manorial expenses and receipts. Totals ('Summa', abbreviated here as 'Sm') are given at the end of each section, with a grand total at the end. The whole compotus gives an idea of the wealth of the manor.

Charge and discharge accounting

Charge and discharge was the most common form of accounting used by landed estates, government departments and public institutions until the mid-nineteenth century. It was a simple overview of receipts and expenditure over the course of a fixed period of time, usually a year. Many accounts covered the period from Michaelmas (29 September) to the following Michaelmas, or Lady Day (25 March) to the following Lady Day. Accounts of income and expenditure in manors or landed estates would have been kept by the steward or bailiff.

The Charge side of the account recorded all the money expected to be received during the period, such as rents, sales, fines paid to the manorial court, and the balance for the previous year. The Discharge side of the account recorded all the money paid out, such as wages, renovations, or the cost of purchasing new livestock.

Charge and discharge was a simple, single-entry system of accounting based on cash transactions. Each transaction was recorded as it happened, and then abstracted to form part of the final account. It did not normally take account of the value of assets, investments, or any other long-term financial entity which might affect the estate or department. It was used more as a check to make sure that the steward or government employee could account for what money he had received, and where it had been spent.

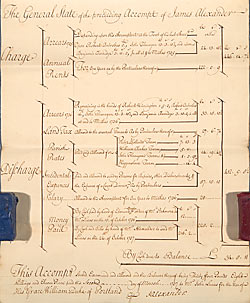

Page from estate account and rental for the manor of Dracklow and Rudheath, Cheshire, 1736 (Pl E 4/1/20/1)

View larger version

This example is the final summary account page drawn up by James Alexander for the manor of Dracklow and Rudheath in Cheshire, for the year ending Michaelmas 1736. The Charge includes arrears and annual rents, and the Discharge includes payments for land tax, parish rates, incidental expenses, salaries and other money paid out. The difference between the two sides of the account goes forward as a balance to the next year's account.

Unfortunately not all charge and discharge accounts use the words 'charge' and 'discharge' so prominently to help with identification!

Other accounting papers in estate collections

Bill for labourers on the Wimpole estate, Cambridgeshire, 1733 (Pl C 1/396)

View larger version

Many details about people living and working on landed estates can be found in estate rentals and bills. The financial prospects of ordinary country people were greatly improved by proximity to a great house. Many farmers had other trades or crafts which could be used by the landlord, thus supplementing their income. Other people were employed as servants or labourers on the estate and enjoyed a regular wage. In return, the landlord depended on local people for fresh produce and manpower.

This account shows the money owed by Edward, Lord Harley, for such services at Wimpole Hall in Cambridgeshire in 1723. The account gives the name of the workman and sometimes his trade (for example, John Elsom, smith and farrier; Mr Stamford for cooper's goods); the amount of bills owing - that is, bills submitted by the workmen which were still to be paid by Lord Harley; the amount of bills which had already been paid in part; and the total due now from Lord Harley to the various workmen. The total amount of bills charged to Lord Harley was £1,132 8s 5½d. Researchers would need to check the complete estate accounts for the Wimpole estate to see if this figure was representative, or if an unusual amount of building or renovation work was being undertaken in 1723.

Next page: Business Accounts